Buying a car shouldn’t feel like a gamble. Yet every year, thousands of people walk away from a dealership with a vehicle that has hidden problems, inflated prices, or undisclosed damage-all because they didn’t know what dealers are legally required to tell them. The truth is, federal and state laws exist to protect you. But knowing those rules isn’t automatic. You have to ask. You have to check. And you have to understand what’s written on the paperwork before you sign.

What Dealers Must Disclose by Law

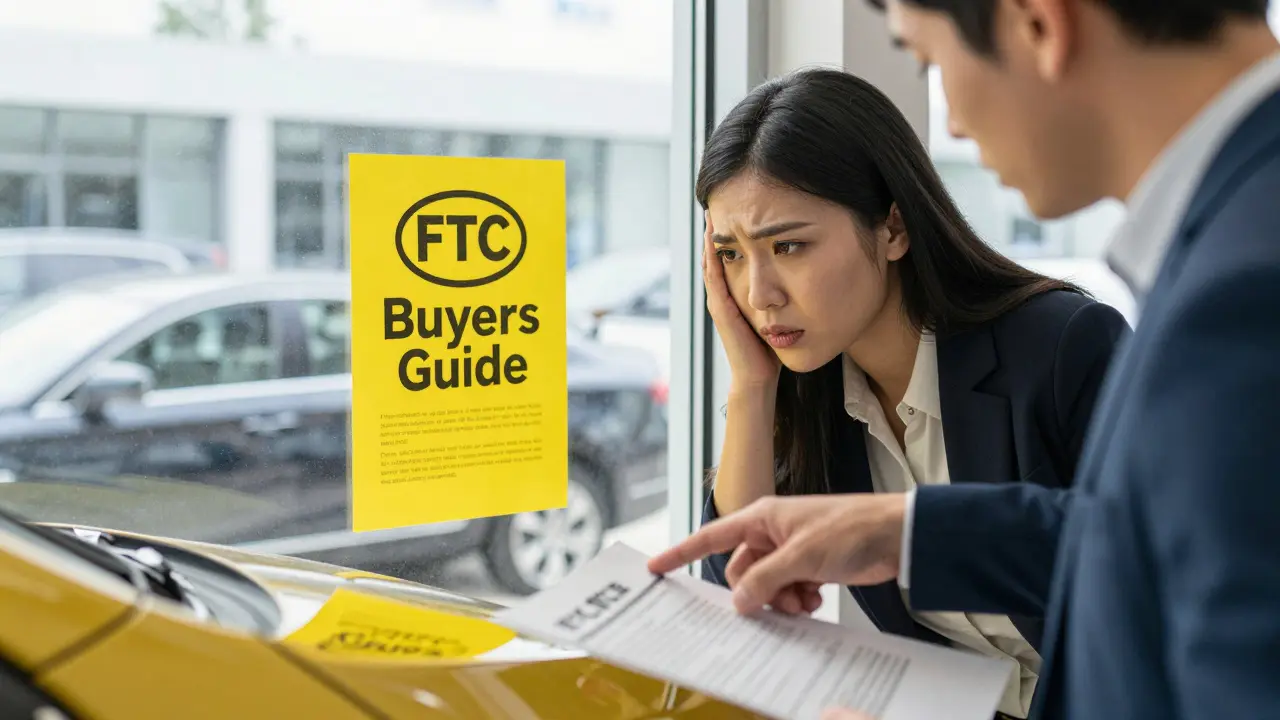

When you buy a vehicle from a dealer, they’re not just selling you a car-they’re giving you a legal contract. And that contract comes with mandatory disclosures. The most important federal rule is the Used Car Rule, enforced by the Federal Trade Commission (FTC). Every used car sold by a dealer must have a Buyers Guide attached to the window. This yellow form isn’t optional. It’s the law.

The Buyers Guide tells you three critical things: whether the car comes with a warranty, what parts are covered if it does, and whether the vehicle is being sold "as is." If it says "as is," that means no repairs are covered after you drive off the lot. No exceptions. No verbal promises. If the salesperson says, "We’ll fix the transmission if it goes out," that means nothing unless it’s written on the Buyers Guide.

Dealers must also disclose any major repairs done to the vehicle in the last 12 months, especially if they cost more than 10% of the car’s current value. That includes engine replacements, transmission rebuilds, or frame straightening. If a car was in a serious accident and repaired, the dealer must say so-unless the repair was minor and didn’t affect safety or value. But if it did? You have the right to know.

Salvage and Rebuilt Titles

One of the biggest traps for buyers is a car with a salvage or rebuilt title. These aren’t just minor issues-they’re red flags that mean the vehicle was declared a total loss by an insurance company, usually after an accident, flood, or fire. In most states, dealers are required to clearly state if a vehicle has a salvage, rebuilt, or flood title. If they don’t, they’re breaking the law.

Here’s what those titles mean in practice:

- Salvage title: The car was damaged so badly the insurer paid out its full value. It’s not legal to drive until it’s repaired and inspected.

- Rebuilt title: The car was fixed and passed a state inspection. But even after repair, it may have hidden electrical, structural, or safety issues.

- Flood title: Water damage can destroy electronics, cause mold, and lead to rust that won’t show up for years.

Some dealers try to hide these titles by selling out-of-state or using temporary tags. Always ask for the title before you pay. Run the VIN through a free service like NICB’s VINCheck. If the dealer refuses to show you the title, walk away.

Odometer Fraud and False Mileage Claims

Mileage is one of the most important factors in a car’s value. But it’s also one of the easiest things to lie about. Federal law requires dealers to disclose the actual mileage on the odometer. They must also sign a statement saying they don’t know of any discrepancies. If they roll back the odometer or claim the mileage is unknown without proof, they’re committing a federal crime.

How do you catch it? Compare the mileage on the title, the Buyers Guide, and the service records. If the car shows 45,000 miles on the window sticker but the title says 89,000, that’s a red flag. Look for wear on the pedals, steering wheel, and driver’s seat that doesn’t match the claimed mileage. If something feels off, get an independent inspection.

Dealers who falsify odometer readings can face fines up to $10,000 per vehicle and criminal charges. But that doesn’t help you if you’ve already bought the car. Prevention is your only defense.

Additional Fees and Hidden Costs

Dealers can’t just add fees without telling you. The Truth in Lending Act and state consumer protection laws require them to list every charge in writing before you sign. That includes documentation fees, dealer prep charges, advertising fees, and extended warranty costs.

Some of these are legitimate. A documentation fee (often called a "doc fee") is common and regulated in most states-it’s usually capped between $100 and $500. But others? They’re scams. A "dealer prep" fee of $800 for washing and vacuuming? That’s not normal. An "advertising fee" you never agreed to? That’s illegal.

Always ask for a line-by-line breakdown of every charge on the contract. If something isn’t explained, refuse to sign. You have the right to negotiate or remove any fee you don’t understand. Many dealers will drop unnecessary charges if you push back.

Warranty Disclosures and Extended Service Plans

If a dealer offers a warranty, they must tell you exactly what’s covered, for how long, and what voids it. No vague promises like "we’ll take care of you." The terms must be in writing. The same goes for extended warranties sold on the lot. These are often overpriced and full of loopholes.

Look for these red flags:

- Warranties that only cover "mechanical breakdowns" without listing specific parts

- Exclusions for wear-and-tear items like brakes, tires, or batteries

- Requirements to service the car only at the dealership to keep the warranty valid

Most extended warranties are profitable for the dealer, not you. The average cost is $1,500-$2,500. The average payout is under $500. If you’re buying a reliable car with low mileage, you’re often better off saving that money in a repair fund.

State-Specific Rules You Can’t Ignore

Federal law sets the floor, but states set the ceiling. Some states have stricter rules than others. For example:

- In California, dealers must disclose if a vehicle has ever been in a hailstorm or fire, even if it wasn’t totaled.

- In New York, dealers must give buyers a 2-day right to cancel for any used car under $40,000.

- In Texas, dealers must provide a written inspection report if the car is over 7 years old.

- In Florida, you can sue a dealer for hiding a salvage title-even if you signed the paperwork.

Don’t assume the rules are the same everywhere. Before you buy, check your state’s attorney general website or consumer protection office. They usually have free guides for car buyers.

What to Do If a Dealer Breaks the Rules

If you find out a dealer hid a flood title, rolled back the odometer, or added illegal fees, you have rights. First, gather all your paperwork: the Buyers Guide, contract, receipts, emails, and any notes from conversations.

Then, file a complaint with your state’s attorney general’s office and the FTC. Most states have a dedicated auto fraud unit. You can also file with the Better Business Bureau. If the amount is over $5,000, consider small claims court. You don’t need a lawyer-you just need the evidence.

Some buyers have won refunds, repairs, or even triple damages under state lemon laws or consumer fraud statutes. But you won’t get anything if you don’t act. The clock starts ticking the day you sign.

Checklist: What to Verify Before Signing

Before you hand over your money, use this checklist:

- Is the Buyers Guide attached to the window? Does it say "as is" or list a warranty?

- Does the title match the VIN on the car? Is it clean, salvage, or rebuilt?

- Is the odometer reading consistent across the title, Buyers Guide, and service records?

- Are all fees itemized and explained? Are any charges missing from the contract?

- Does the warranty document list covered parts, duration, and exclusions?

- Did you get a copy of everything you signed?

If even one item is missing or unclear, don’t sign. Walk out. Come back tomorrow. Or go to another dealer. There are thousands of cars on the market. You don’t need to buy this one.

Final Thought: Knowledge Is Your Best Protection

Dealers aren’t evil. Most are just trying to make a sale. But the system is built to favor the seller unless you know your rights. The law gives you power-but only if you use it. Don’t trust words. Trust paper. Don’t believe promises. Check the facts. Ask for proof. And never, ever sign anything you don’t fully understand.

Buying a car is one of the biggest purchases you’ll ever make. Don’t let a lack of information cost you thousands-or your safety. Know the rules. Ask the questions. Walk away if needed. Your future self will thank you.

Do dealers have to disclose if a car was in an accident?

Yes, if the damage was significant enough to be reported to an insurance company or affect the vehicle’s safety or value. Most states require dealers to disclose major accident history, especially if the car received a salvage or rebuilt title. Minor dents or scratches that were repaired without insurance claims don’t always need to be disclosed, but major structural damage does.

Can a dealer sell a car "as is" and still offer a warranty?

No. If a vehicle is sold "as is," it means no warranty is included-by law. The Buyers Guide must clearly state this. If a dealer claims they’ll fix something after the sale but doesn’t put it in writing on the Buyers Guide, that promise isn’t legally binding. You can’t have both "as is" and a warranty on the same sale.

What’s the difference between a salvage title and a rebuilt title?

A salvage title means the vehicle was declared a total loss by an insurance company and hasn’t been repaired yet. It’s not legal to drive. A rebuilt title means the vehicle was repaired, passed a state inspection, and is now legal to drive. But even with a rebuilt title, the car may have hidden issues from the original damage.

Are extended warranties worth buying from a dealer?

Usually not. Extended warranties sold by dealers are often overpriced and come with strict exclusions. The average payout is far less than the cost. If the car is reliable and under factory warranty, it’s often smarter to save the money in a repair fund. Only consider one if the car is high-maintenance, out of warranty, and you can’t afford unexpected repairs.

Can I cancel a car purchase after signing the contract?

In most states, no-once you sign, the deal is final. But a few states like New York and California offer a short cooling-off period (usually 2-3 days) for used cars under a certain price. Always ask about cancellation rights before signing. If the dealer didn’t tell you about one, you may have legal recourse.

Teja kumar Baliga

December 20, 2025 AT 09:26Just bought my first car last month and this post saved me so much stress. I asked for the Buyers Guide like it said and noticed the "as is" tag-walked away when they tried to upsell me on a warranty. Best decision ever.

Tiffany Ho

December 20, 2025 AT 12:45thank you for this i read it all and now i feel less scared about buying a car

Alan Crierie

December 20, 2025 AT 17:55Love how you broke this down. So many people don’t realize the Buyers Guide is legally binding. I always print mine out and keep it with my title now. Small habit, huge protection.

Nicholas Zeitler

December 21, 2025 AT 18:55Don’t forget to check the NHTSA recall database too! Even if the dealer says "no recalls," run the VIN yourself. I caught a hidden airbag issue that way-saved my life.

lucia burton

December 22, 2025 AT 07:54Let me just say, as someone who’s worked in dealership compliance for 12 years, the level of ignorance among consumers is staggering. Dealers are trained to exploit ambiguity in language-"extended service plan" vs. "warranty," "pre-delivery inspection" vs. "dealer prep fee." They’re not lying, they’re linguistically obfuscating. And if you don’t know the difference between a salvage title and a rebuilt one, you’re already in the meat grinder. This isn’t about being paranoid-it’s about understanding the architecture of predatory sales tactics. You want to walk away with a car? Then you need to understand the legal scaffolding that’s supposed to protect you-and then demand it be enforced.

Zelda Breach

December 23, 2025 AT 12:13Oh wow, so the "dealer prep" fee is just them charging you to wash the car they already washed before you even walked in? Brilliant. I’m calling my state AG tomorrow.

Aryan Gupta

December 25, 2025 AT 09:28Wait, you mean dealers can legally hide flood damage if they sell out of state? That’s not a loophole-that’s organized fraud. And the FTC? They’re a joke. I’ve seen cars with 300K miles that were rebuilt after a tsunami. No one checks VINs. No one cares. This is why America’s roads are death traps.

Gareth Hobbs

December 26, 2025 AT 19:47Yea right. "Check the title" lol. Like some guy in a flannel shirt is gonna know what a rebuilt title looks like. And the FTC? Ha. They got 12 people working on auto fraud. Meanwhile, dealers are hiring ex-cops as "compliance officers" to look legit. This whole system is rigged. And don’t even get me started on how they use temporary tags to dodge state inspections. It’s a national scam.

Denise Young

December 27, 2025 AT 01:41Let’s be real-extended warranties are the dealership’s profit engine. They make more off those than the car itself. I used to work in finance at a Toyota lot. The numbers don’t lie: 87% of extended warranty claims are for things like radio buttons and AC vents. You’re paying for a luxury, not protection. Save the cash. Buy a good car. Done.

k arnold

December 27, 2025 AT 12:35Wow. A 12-page essay on how to not get scammed. Congrats, you just described the entire used car industry. What’s next? A 50-page guide on how to not get punched in the face at a bar?

Kelley Nelson

December 27, 2025 AT 15:13It is, of course, profoundly regressive that the onus of legal literacy falls entirely upon the consumer in a transaction of such magnitude. One might reasonably expect that the burden of transparency would rest with the seller, particularly when the asymmetry of information is so grossly disproportionate. The very existence of the Buyers Guide-as a mandatory, standardized disclosure-is a tacit admission of systemic malfeasance. Yet, we are told to "ask"-as if inquiry were a sufficient bulwark against institutionalized deception.

Sam Rittenhouse

December 28, 2025 AT 16:56I’ve seen people cry after buying a car that broke down two weeks later because they didn’t check the title. Don’t be that person. Take your time. Bring a friend. Ask for everything in writing. It’s not just money-it’s your peace of mind. You deserve better than a gamble.

michael Melanson

December 30, 2025 AT 06:06Good stuff. I always run the VIN on Carfax and then double-check with NICB. If they don’t match, walk. No exceptions.

Fredda Freyer

December 31, 2025 AT 10:30There’s a deeper truth here: buying a car isn’t a transaction-it’s a ritual of trust. And we’ve built a system where trust is the liability of the buyer, not the seller. The law gives us tools, yes, but it doesn’t change the psychology. We want to believe the salesperson. We want to feel safe. But safety doesn’t come from smiles-it comes from paper, signatures, and the courage to say "no" when your gut screams. This isn’t just about cars. It’s about reclaiming agency in a world that wants you to be passive. So ask. Check. Walk away. That’s not being difficult. That’s being human.